A Comprehensive Guide to Vehicle Repossession In Georgia

Helping You Rebuild Financial Freedom

The Basics of Vehicle Repossession In Georgia

If you are facing the possibility of vehicle repossession in Georgia, you may have legal options. Find out everything you need to know about vehicle repossession and how to stop it here.

Vehicle repossession refers to a non-negotiable act by an auto lender of taking possession of your car due to delayed car payments. Sometimes it also involves the lender auctioning your car and tasking the money to the debtor’s loan.

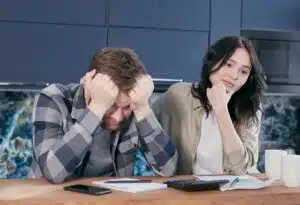

Facing repossession is very overwhelming. Not only does it inconvenience your way of transportation, but it also damages your credit score as well.

To avoid this from taking place, you certainly should take steps to stop it. Here’s what you need to know about how to stop and avoid the repossession process.

What Are The Vehicle Repossession Laws In Georgia?

If you miss making your car payments or default on your loan, there are higher possibilities you are at risk of getting your car repossessed by your creditor. Several laws govern repossession. If you face car repossession, it’s best to consult an Alpharetta bankruptcy lawyer for legal advice.

Some of the repossession laws in Georgia include:

A Creditor Can Sue Or Repossess Your Vehicle

Under Georgia state laws, if you delay your car payments or your loan contract defaults, the car lender has the right to repossess the car. The creditor can take your car once you default on the debt or even go to the extent of suing you for the remaining debt you owe them.

A Creditor Can Garnish Your Wages

A creditor or a lending company is allowed to levy your bank accounts to try and compensate the debt for the repossessed vehicle.

The Vehicle Must Be Repossessed Without A Breach of Peace

The vehicle must be repossessed without involving any chaos. According to Georgia laws, as long as the repossession agent doesn’t breach the peace or take the property by force, it’s regarded as perfectly legal.

The Lender Can Sue You For The Deficiency Amount

In Georgia, a car creditor must notify you within ten days from the day of repossession. But if you decline to do so, the lender is obliged to take the vehicle back to sell it or auction it. However, if the car sells for less than you still owe, the creditor will come for the deficiency balance. Also, when a borrower leases a car, a loan agreement should be signed to state that the remaining loan balance will be paid back in installments.

The Vehicle Repossession Process In Georgia

The repossession process relies on the jurisdiction. But in most circumstances, a lender can repossess your car any time after a failed payment. Usually, no notification is given. A repossession company will come to collect the vehicle but exceptionally without causing any damages.

Once it’s finally repossessed, the creditor eventually sells it to an auction to redeem as much as possible of the balance on the pending loan. However, the vehicle must be sold in a commercially reasonable manner and at a fair market price. From there, the creditor must notify you of the time and place your car has been sold.

Reasons For Vehicle Repossession In GA

When a car is repossessed, it is usually because of failed or missed payments on your auto loan. Once the loan and grace period has depleted, the creditor has the right to take away your car, and at most times, it usually occurs without any notice or even without a court order. It may also result in creditors selling your car contract to another person. You may consider contacting a bankruptcy lawyer for legal help and potentially get your car back.

Some of the reasons that may lead to car repossession include:

Late And Missed Payments

Failing to make your payments on the due date may be considered a default on the contract. Once the contract is regarded as default, a car creditor can repossess the vehicle at any time.

Inadequate Insurance

Failing to have the proper insurance or allowing your insurance coverage to slip may be regarded as a default. This may cause your vehicle to be repossessed.

Car Repairs

In some instances, failing to pay your repair charges on the agreed time can force a mechanic to call a creditor on you. A creditor might be coerced to repossess the vehicle to avoid the mechanic or body shop from making a legal claim. Ultimately, this might force you to pay for the repair cost and the amount related to keeping your car.

How To Avoid Car Repossession In Georgia

Dealing with car repossession can negatively impact your finances. Not only does it affect your daily life activities, but it greatly damages your credit score and even makes it hard to be certified for credit in the future.

Therefore, it’s imperative to understand your options for possibly avoiding car repossession. Below are some potential ways that debtors may avoid repossession.

Communicate With Your Lender

Always reach out to your lender to establish other options whenever you suspect you might miss a car payment. Repossession is very expensive, so keeping your loan in a good reputation could be a go-to option for you and the lender as well.

Some options that are worth going for include a modified payment program and paused payments through fortitude.

Refinance Your Loan

If you are behind your payments, repossession is a likely possibility. This could call for you to opt for refinancing your car loan. By doing this, your new loan will be used to clear the existing one, and it will allow you to begin afresh.

However, it’s important to note that refinancing is just a short-term solution, and it won’t help in the long-term payment problems. It’s a smart decision only when you are confident that you’ll be able to make your payments on due time.

Voluntary Sell The Car Yourself

Voluntarily surrendering your vehicle could be the last decision you will make. It will still damage your credit score but not as much as the repossession. Additionally, a voluntary repossession of your car could assist you in getting more money than what the creditor would have obtained if the vehicle was sold at auction since the creditor won’t have to hire a repo company to seize your car. Depending on your particular situation, this could help you to pay off your outstanding loans and solve any other pending financial situation.

File Chapter 13 Bankruptcy

When filing Chapter 13 bankruptcy in Georgia, your creditor is forbidden from repossessing your motor vehicle. In other words, Chapter 13 bankruptcy can be a way to stop repossession since the automatic stay will protect your car while your case is active.

Under some circumstances, filing a Chapter 13 bankruptcy can even be a way to get your car back after it has already been repossessed. Under Georgia law (O.C.G.A. 10-1-36) that provides the rights of the buyer and seller after the repossession of a motor vehicle sold under a retail installment contract, you can redeem your car after repossession as long as you do so within ten days of the repossession. So, filing bankruptcy within ten days after repossession may be a good way to regain your car.

If you don’t respond within that 10-day period, the repossessed motor vehicle can be auctioned or sold off by the repossession company or the creditor.

Contact a Lawyer to Learn More About Georgia Repossession Laws If You Are Behind On Your Car Loan Payments

Cars are one of the most common assets that get caught up in repossession. But it may also include other property and personal items such as real estate or any tangible asset. If you face repossession or your vehicle has already been auctioned, you can contact a bankruptcy attorney for legal advice and discuss your options. Our law firm offers a free consultation to prospective clients, so exploring your options is risk-free.

Frequently Asked Questions

Under Georgia law, a creditor can repossess a vehicle as soon as a borrower defaults on the loan contract, which most commonly occurs after a single missed or late payment. Lenders are generally not required to provide advance notice or obtain a court order before seizing the vehicle.