What is a Credit Score

A credit score is a mathematical algorithm, typically updated monthly, used by lenders and service providers (i.e. utility companies) to determine your character, creditworthiness, and likelihood to make payments on time.

Read more on:

Prior to the universal adoption of the FICO score in 1989, bankers would make a decision to lend money based on a “gut feeling”. Obtaining credit was all about who you knew. Many people were denied credit based on gender, race, nationality and marital status.

Conversely, the current credit score model allows any lender to obtain a picture of your current debts with outstanding balances, along with your repayment history.

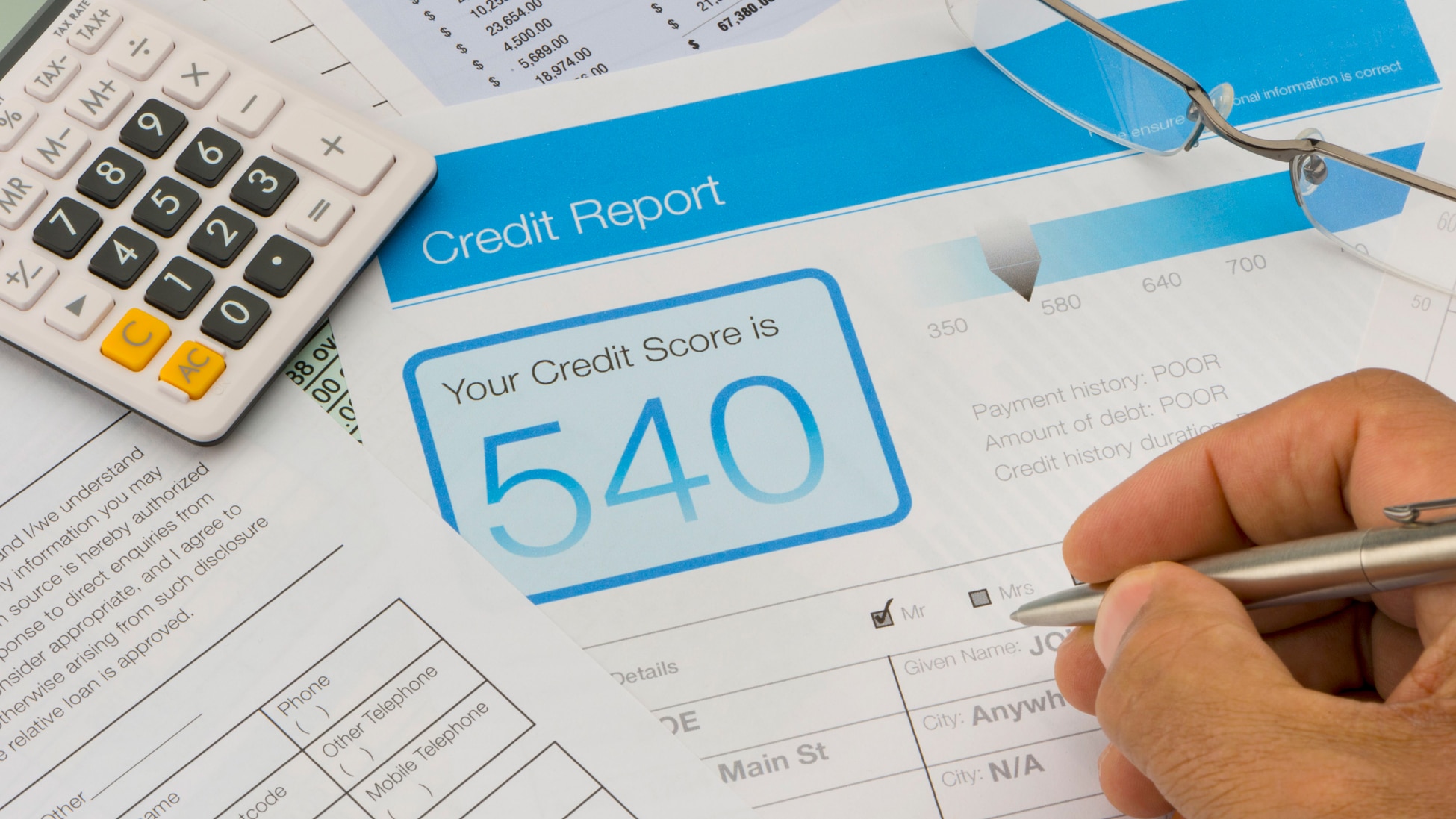

Credit Bureaus and Credit Scores

While a credit score is a number, the data (your individual credit history) used to create is the score is provided to the bank or credit card company from a credit referencing agency, also known as a credit bureau.

Experian, Equifax, and TransUnion are the credit bureaus that compile your financial history and share this history with lenders by request.

Credit scores may vary slightly based on the credit bureau or lender that completed the calculation.

Improve your Credit Score

Lower credit scores can reduce your odds of being credit approved. A “good” credit score is typically over 700 (on a scale out of 850). If your credit score is not as high as you desire, follow these steps to increase your score:

Dispute any incorrect findings

Make all payments on time

Pay off debt

Keep credit card balances low

Maintain a credit utilization of under 30%

Credit utilization is your total debt divided by total available credit

Assess unused credit card accounts

Only close accounts if doing so will increase credit utilization %

Fewer open accounts with the same overall debt may lower your score

Check Your Credit Report for Free

Visit Experian to check your credit report for free. Checking your own credit is a soft inquiry. Soft inquiries do NOT impact your credit score.

An updated free credit report can be accessed every 30 days. Outstanding balances on credit cards and loans will be reflected as well.

Monitoring your credit report allows you actively increase your score while becoming a more informed applicant.

Additionally, you can obtain a FREE credit score.

Bankruptcy and Your Credit Score

Chapter 7 and Chapter 13 can remain on your credit report 10 years. That being said, the three major credit reporting agencies voluntarily remove Chapter 13 bankruptcies after seven years. Chapter 7 bankruptcies remain on your credit report for the full ten years.

Read more on: the differences between Chapter 7 and Chapter 13

Filing for bankruptcy does not mean you are “doomed” for seven to ten years. A large majority of people notice an increase in the credit score within 12 months of filing for bankruptcy. This is a result of discharged debt and making payments on times.

Consult a Bankruptcy Attorney

The office of Cherney Law Firm LLC is committed to helping you get your finances and credit score back on track. Contact us at 770-415-3253 to schedule a free consultation to learn how bankruptcy can help you.

Matthew Cherney

Website: https://cherneylaw.com

At Cherney Law Firm LLC, clients can expect the highest quality legal representation alongside thoughtful counseling and attention to detail. Mr. Cherney dedicates his time to properly investigating every possible avenue of debt relief for his clients before simply stepping into bankruptcy. Seeking to make each consumer that comes to him for legal aid as comfortable as possible, he keeps his clients in the loop with every step he takes.